On a Parity PEG basis, there seems to be reasonable potential here for a conservative 2 Year upside of 100%

Companies: Volex plc

Volex, ticker VLX, manufactures and supplies power cords and cables across a variety of industries.

The following provides an analysis and view of this company based on…

- Data obtained from Stockopedia

- The most recent Broker note from Research Tree and

- The Parity PEG Price Report produced by Briefed Up

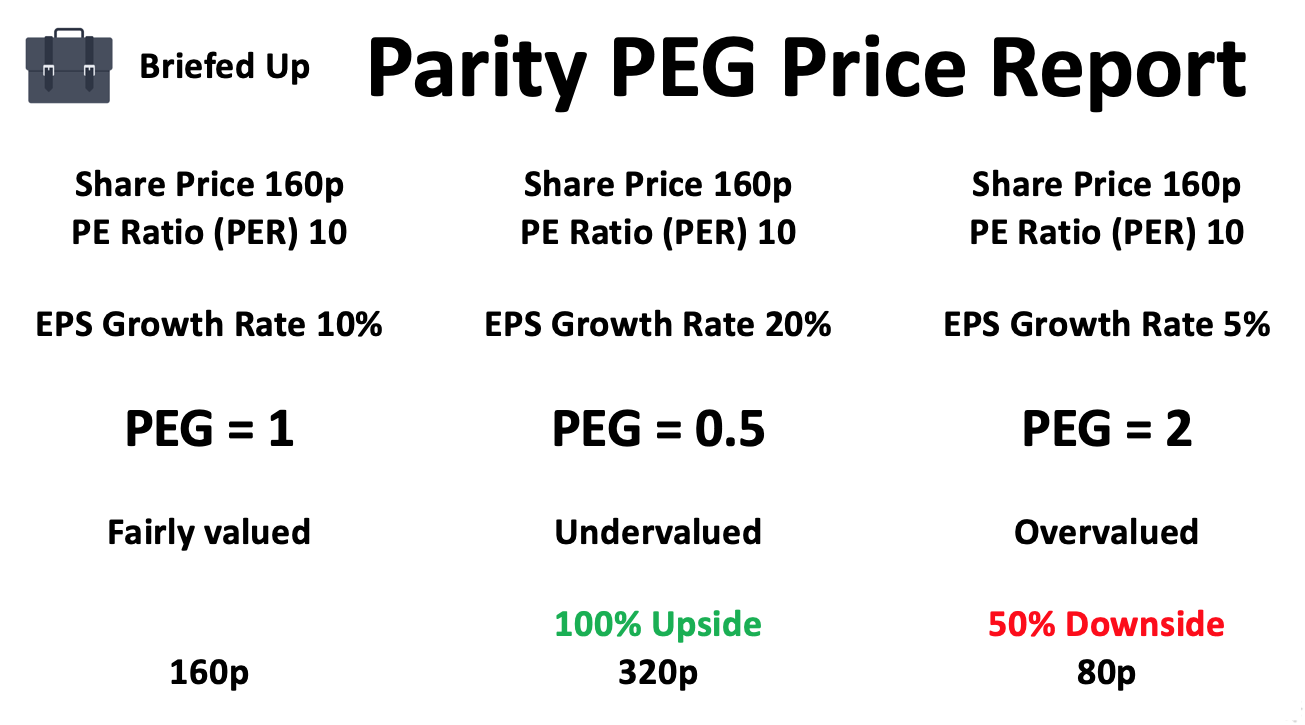

The primary focus of the Parity PEG Price Report is the PEG Ratio, the PEG. The objective is to identify a 1 and 2 Year fair value price based on the PEG and the forecast EPS growth.

The PEG was made popular by Peter Lynch. It is calculated by dividing the PE Ratio, the PER, by the EPS Growth Rate.

A PEG of 1 indicates a stock is fairly valued, a PEG below 1 indicates a stock is undervalued and a PEG above 1 indicates a stock is overvalued.

Thus, a stock with a PER of 10 and an EPS Growth Rate of 10% would have a PEG of 1 and would be considered fair value.

A stock with a PER of 10 and an EPS Growth Rate of 20% would have a PEG of 0.5 and would be considered undervalued with 100% Upside – Where the PEG would then be at parity.

A stock with a PER of 10 and an EPS Growth Rate of 5% would have a PEG of 2 and would be considered overvalued with 50% Downside - Where the PEG would then be at parity.

Onto the analysis and view…

This is a company I actually bought into late last year at 88p and the current Market Cap is £136m.

There was a lot to like back then and there’s still a lot to like now.

There’s Net Cash, about 10% or so of the current Market Cap and there’s a decent 3% yield.

Technically, there’s arguably a 1 year Uptrend. Perhaps it’s more reasonable to say that price has been moving upwards in a range between 75p and 100p or so.

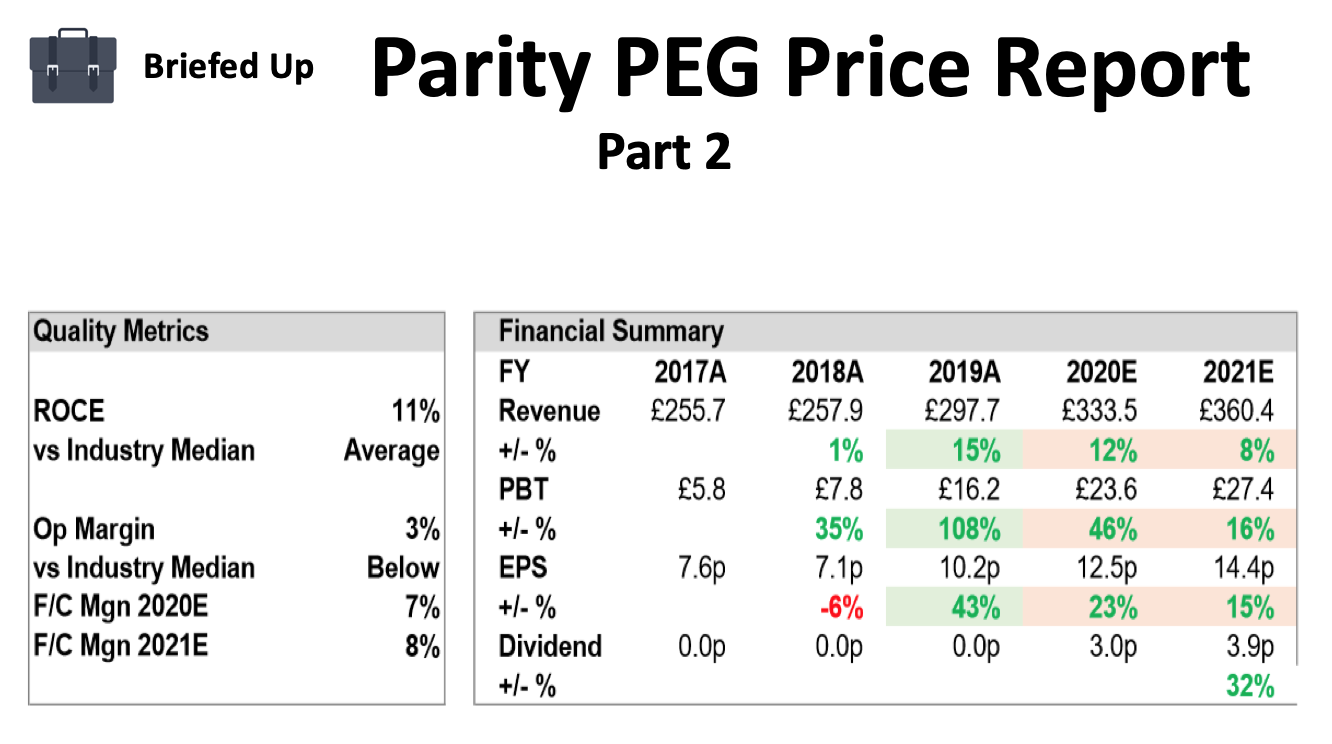

The Quality Metrics

Both the ROCE and Operating Margin figures are taken from Stockopedia. The ROCE is not great at 11% but it is about average for the industry. The Operating Margin is not great either, at 3%, as it’s below the Industry Median. However, the latter is forecast to rise to 7% and 8% in 2020E and 2021 respectively which is more in-line with the Industry Median.

The Financial Summary

All figures here are taken from the most recent Broker note from N+1 Singer on 30th July 2019.

Revenue is forecast to increase by 12% in 2020E but then slow to 8% in 2021E. With help from the improvement in those margins mentioned previously though it means that PBT is expected to grow 46% and 16% respectively with EPS at 23% and 15%.

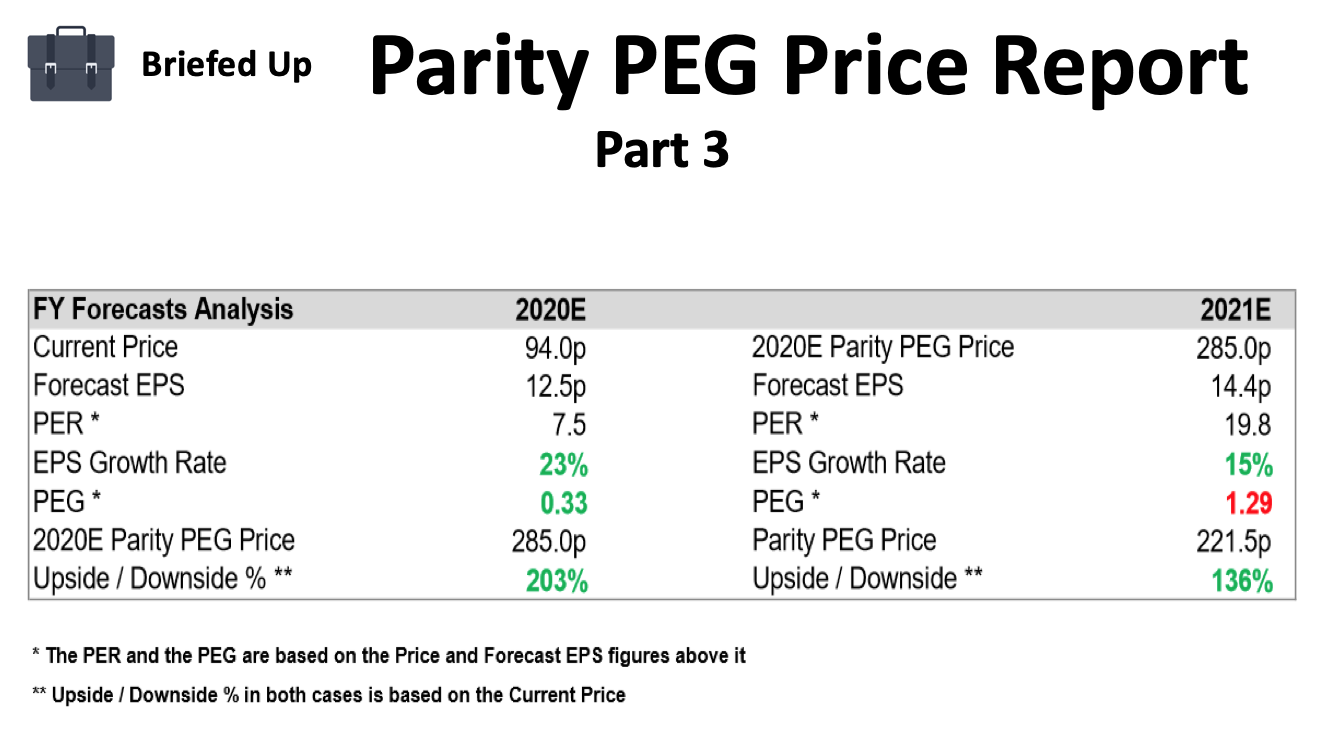

Forecasts And PEG Analysis

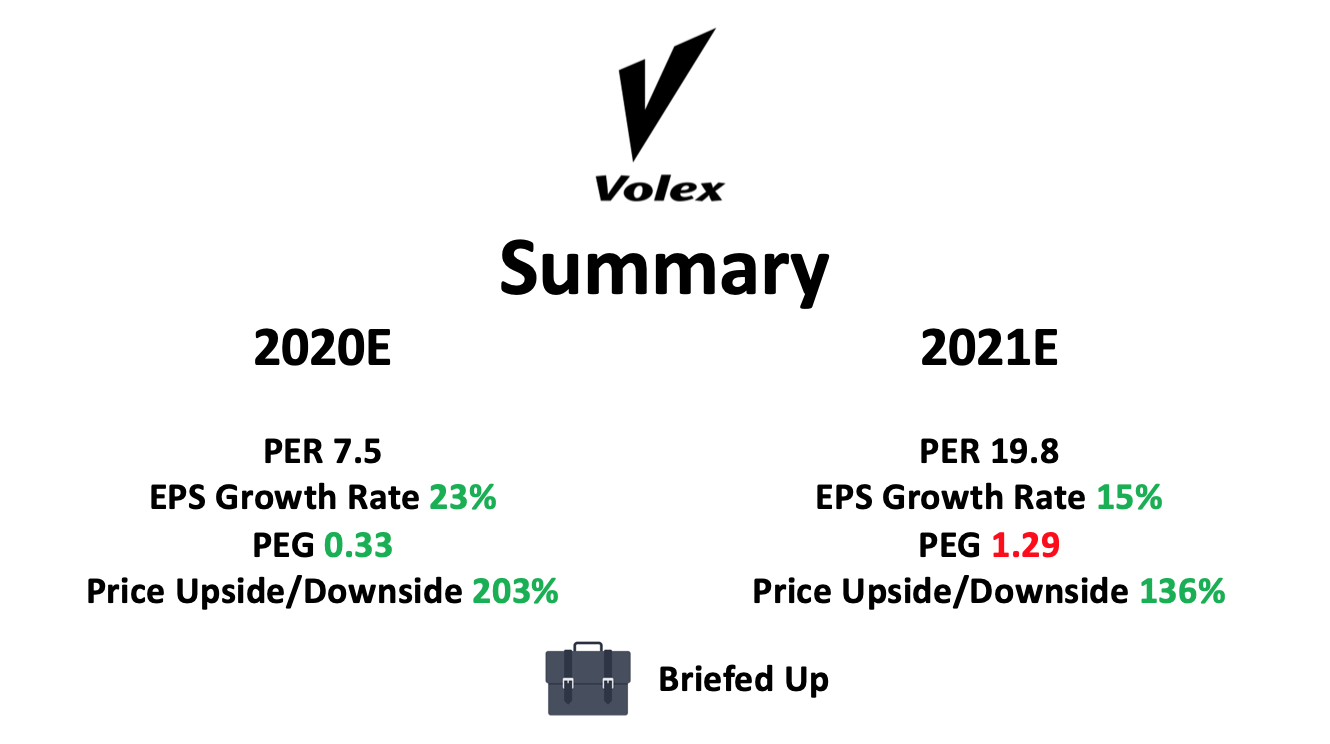

Looking at 2020E there’s a forecast PER of 7.5 and EPS growth of 23%. This translates to a PEG of 0.33 and a potential upside of just over 200% from the current price level (on a Parity PEG basis).

Looking to 2021E there’s a forecast PER of 19.8 and EPS growth of 15%. This translates to a higher PEG of 1.29 and thus reduces the potential upside to 136% from the current price level (again, on a Parity PEG basis).

These estimates could perhaps be considered a little conservative based on the fact that the Industry Median PEG here is 1.18.

To, summarise…

On a Parity PEG basis, there seems to be reasonable potential here for a conservative 2 Year upside of 100%.

And, that’s without taking into account the Net Cash of 10% or so of the current Market Cap (which could be returned to shareholders or, preferably, used for additional earnings enhancing acquisitions) and the decent 3% yield.

This analysis and this view is of course no recommendation to Buy or Sell shares in Volex and does not cover any risks associated with investing in this company or any other company.

Hope it helps!

You can see many more reports on our website https://briefedup.com/.

Please Note: These reports are purely my opinions at that point in time on stocks I may or may not have a position in. I do not and will not ever give any advice. As always, do your own research.