Has the big rotation out of Bond Proxies into Cyclicals begun?

Companies: BHP Group Ltd, Reckitt Benckiser Group plc

I'm a fund manager working in the city and focused on UK small and mid-cap companies. I've managed money there for most of the last decade and before that worked as a buyside analyst.

It's fair to say there is a host of myths and misconceptions about the industry in which I work. Some of it is encouraged to build mystique and therefore brand. Some, in my humble opinion, comes from a lack of transparency when looking from the outside.

I'd been thinking about capturing my thoughts periodically for a few years now, mainly to help focus my views about markets. So when the guys at Research Tree approached me about a weekly column, it felt like the right time to start.

My 5 point mission statement for this column:

Only write down stuff I find interesting - If I don't think it's interesting you certainly won't so why waste everyone's time?

Be brief! - Like all fund managers, I get bombarded with information all day, much could be written in half the words (and some not at all).

Be clear how I think about stocks - I promise to try not to bore but I thought it necessary to give an idea of my process (see below).

Share what I've learnt (or re-learnt) that week - This includes actions by corporates that annoy or impress me, red flags, funny anecdotes, interesting themes, etc.

Remain anonymous - Sorry I know this might irritate some readers, but I genuinely think I can be more honest, less guarded and therefore more interesting if I maintain anonymity.

How I think about valuation

I've always been an unabashed borrower of other people's good ideas. And there's no shame in using a philosophy that has worked for other people as a starting point for managing your own investments. I try to manage my fund using a combination of growth, value and quality principles. The investors that I try to emulate are Greenblatt, Klarman, Lynch and Buffett. That's a very easy sentence to write but a tough job to implement.

I use various screens as a starting point:

High Return on Capital Employed and Earnings Yield are important metrics to narrow down my efforts to companies with high-quality earnings engines that trade at reasonable prices (a la Greenblatt).

High Operating Margins and Operating Cash Flow help narrow in on companies that can better weather downturns.

These screens give me a shortlist from which the real work begins. I won't pretend that I have in-depth models and valuations for each of the companies on my radar. I'd never see my kids or wife if I did. But you shouldn't need to.

Broker research is always a good starting point in covering the key issues, and I make sure I meet management. My models are simple and quick to update, meaning they're never going to be 100% on the money, but they will capture the essential moving parts and highlight risks and opportunities.

The usual factors I then consider are:

- Management track record,

- Accounting red flags,

- Potential addressable market size, and

- Competitive landscape, among others.

However one other important factor I focus on (thanks to Klarman) is the need to have a big enough market to reinvest in. It's all well and good finding high ROCE companies, but if their niche is too small, the wonders of compounding can never be realised. In these cases, the company normally has to distribute these high returns to shareholders through dividends. This is fine, but compounding is so much better.

And now onto a theme I think is especially interesting right now...

Has the big rotation out of bond-proxies begun?

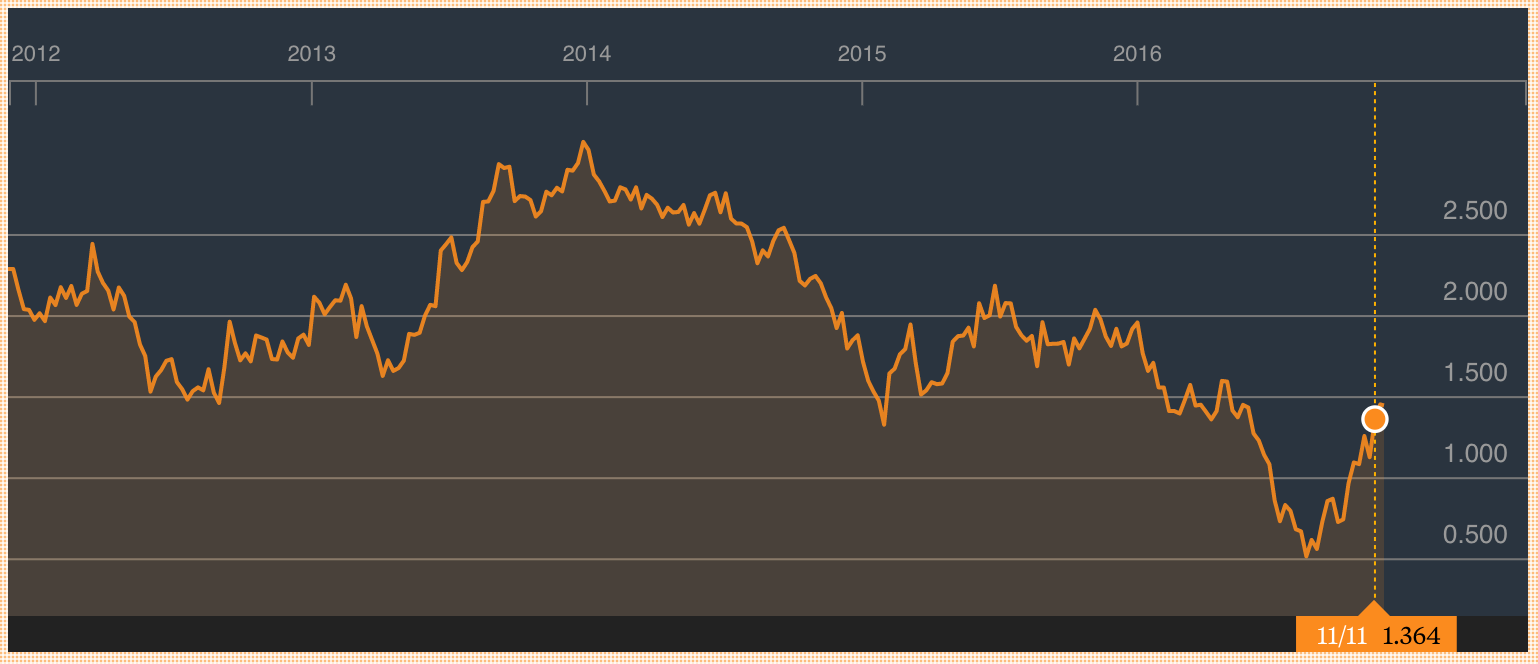

The topics I want to highlight this week are rising yields, the future of bond-proxies/defensive stocks, and whether we are at the tipping point of huge rotation out of Defensives and into Cyclicals. It starts with the chart below but what I find fascinating is the question of whether this recent reversal of a trend that has been in place for the last 5+ years will continue.

In the above 5-year chart, I've picked the well-known defensive name of Reckitts and plotted it against a cyclical stock, BHP Billiton. The orange line is the 10yr UK Gilt yield. I could have chosen many examples, and they would show the same trend. After years of Defensives outperforming Cyclicals, there has been the start of a reversal. Many of these defensives and "bond proxies" are still trading at lofty multiples. For example, Reckitts is trading on a PE ratio of over 31x (trailing 12 months).

What's driving the rotation and will it continue?

Below shows the UK 10yr Government Bond yield for the last five years. It hit all-time lows of 0.5% back in mid-August but has been on a streak ever since. Inflation expectations have returned with the US Fed almost certain to raise rates ahead of the Christmas break, and Brexit will drive inflation even further this side of the pond.

This trend started before Trump was elected but look at recent events. The new-look era of Trumponomics in the US is set to bring a massive increase infrastructure spend. And in little old England, our Chancellor Hammond recently loosened the austerity belt in the Autumn Statement by removing the target to eradicate the deficit by 2020. In short, debt levels are set to rise, inflation looks to be inevitable, and hopefully increased capital investment might herald some proper growth.

Trump's economic adviser Anthony Scaramucci gives an insight into the changes we can now expect in the US:

"Trump would ideally like to see corporate tax rates cut to 15% from 35%."

"Business people like Mr Trump understand you can grow yourself out of excessive debt."

Trump's $1 trillion infrastructure plan will be "financed by historically cheap debt and public-private partnerships"

This is quite a "top-down" theme to start my blog with but in terms of significant financial trends, Defensive stocks offering "bond-proxy" yields have been where an enormous amount of money has been sitting as a result of our ultra-low interest rate world. If yields are rising this could be the start of that trend unwinding. It doesn't take a genius to realise capital flows of that scale would weigh on defensives vs. cyclicals.

-----

Please Note: To be clear, I do not and will not ever give any advice. I will rarely mention individual stocks but when I do these will not be recommendations, instead just my thoughts at that point in time.