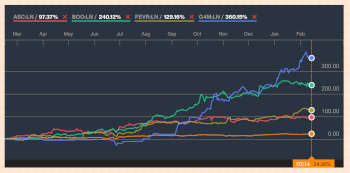

Gear4music reported strong first half sales growth in its trading statement today as both UK and Europe made brisk gains and the combined H1 figure beat current expectations. A higher full year number than originally envisaged seems likely, although the company did encounter some margin pressure. Overall, Gear4music’s growth stock credentials look intact.

_m.jpg)

.png)