Is Q2/H1 relevant? Arguably not

Given the exceptional context, one can validly question whether Q2/H1 trends have any relevance to equity valuations. Notwithstanding this, we thought it a timely juncture to revisit estimates across our Consumer Staples coverage universe.

Where we stand relative to near-term consensus

Relative to near-term consensus expectations (Visible Alpha: Q2/H1), we find ourselves materially below consensus on key metrics for most names. The notable positive exceptions to this being the brewers and Reckitt.

Taking a longer-term perspective: we see scope for relative multiple expansion

Assuming that we will remain in a low rate environment for the foreseeable future, staples look reasonably good value to our eye. Core EU Staples (Food, HPC and Bevs) currently trade at a 27% premium relative to market, albeit against an inflated market P/E. Looking forward to CY21e, we are at a 38% premium and on CY22e, we are at a 49% premium.

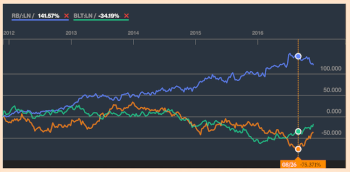

Danone: We downgrade to Neutral

While we believe that Danone is relatively cheap, we increasingly struggle to see what will trigger the market to positively re-appraise. Organic growth in FY20e will likely be lacklustre (0.0%), structural questions will likely only deepen (Waters, Dairy, Chinese IMF), there will be no near-term CMD, Nestle''s US Water disposal is unlikely to be a positive valuation marker and to our mind a portfolio review is all well and good but there is not an obvious SOTP argument. While Danone may be relatively cheap, we suspect it will stay that way. We downgrade to Neutral. TP to EUR66.

We revise target prices across the sector

We revise target prices across the space to reflect both a re-appraisal of our EU Food, HPC and Brewer''s benchmark multiples plus the 6 month roll-forward of our target earnings base. The most noteworthy revisions are at ABInBev (+14%), Danone (-8%), L''Oreal (+12%) and Reckitt (+13%).