25 September 2025

Results for the year ended 30 June 2025

Strong Momentum, Strengthened Solvency, Sustained Dividend and Positive Outlook

Summary

|

|

FY 2025 |

FY 2024 |

|

New business sales - PVNBP 1 basis |

£82.4m |

£77.8m |

|

New business sales - APE 2 basis |

£12.2m |

£10.4m |

|

IFRS profit before tax |

£1.8m |

£5.3m |

|

Underlying profit |

£5.1m |

£8.5m |

|

Recommended final dividend per share 3 |

2.65p |

2.65p |

|

IFRS earnings per share |

1.31p |

3.80p |

|

Solvency ratio |

169% |

149% |

|

As at |

30 June |

30 June |

|

|

2025 |

2024 |

|

Assets under Administration |

£1.13bn |

£1.15bn |

|

Value of In-Force |

£103.1m |

£110.8m |

1 Present Value of New Business Premiums

2 Annual Premium Equivalent

3 Subject to approval at the AGM

"FY 2025 was a year of strategic execution and renewed momentum. We delivered growth in new business, launched award-winning products, and embedded our new policy administration system.

While IFRS profit declined due to continued investment and litigation costs, our underlying performance remains robust, and our solvency position has strengthened to 169%.

We are excited about the opportunities ahead, particularly the launch of our Japanese proposition and further expansion in

NEW BUSINESS

New business for FY 2025 totalled £82.4m on a PVNBP basis, up 5.9% from £77.8m in FY 2024. APE increased by 17.3% to £12.2m, driven by strong uptake of Global Select, a single premium bond, and early traction from Ascend and Future Focus, designed to support regular and flexible premium growth.

Single premium sales rose 72.5% year-on-year, while regular premium sales declined 10.0%, with signs of recovery emerging in the second half. The launch of our Japanese proposition and continued growth in

TRADING RESULTS

IFRS profit before tax was £1.8m (FY 2024: £5.3m), reflecting continued investment in strategic initiatives and elevated litigation defence costs. Underlying profit, excluding non-recurring items, was £5.1m (FY 2024: £8.5m).

Fee and commission income remained stable at £48.2m, supported by strong equity markets and resilient contract holder activity. Investment income rose to £5.0m (FY 2024: £4.7m), benefiting from favourable interest rate conditions and proactive treasury management.

Administrative and other expenses increased to £36.7m (FY 2024: £33.3m), driven by depreciation of the new policy administration system and targeted growth investment.

Value in Force totalled £103.1m as at 30 June 2025 compared to £110.8m at 30 June 2024. This reduction has primarily arisen because the profits earned during the year exceeded the expected future profits from new business written in the same period. We have also revised some assumptions with regards to future policyholder behaviour and expenses which has had a negative impact.

Assets under administration were £1.13bn as at 30 June 2025, down slightly from £1.15bn at 30 June 2024.

policyholder LITIGATION

The Group continues to manage legacy litigation exposures with discipline. As at 30 June 2025, writs served represented a net cumulative exposure of €23.8m (£20.4m), consistent with €23.8m (£20.2m) a year earlier.

Five new writs were received during the year (FY 2024: 12), reflecting a notable decline in new claims and highlighting the maturity of the legacy book.

The Group recorded £0.4m in insurance recoveries and continues to expect that several larger claims will be mitigated through insurance. While resolution timelines vary by jurisdiction, the Group remains confident in its legal defences and anticipates further progress in FY 2026 as claims mature and recoveries advance.

OUTLOOK

FY 2026 represents a pivotal year in Hansard's strategic journey, as the Group transitions from foundational investment to execution and growth.

Our strategy continues to be anchored in three imperatives:

· Improve: Elevate customer service standards and enhance product features to better meet evolving client needs.

· Grow: Launch our Japanese proposition in partnership with Guardian and deepen distributor relationships across

· Future-proof: Optimise operational efficiency, manage legacy litigation, and advance our ESG agenda to ensure long-term resilience and sustainability.

New sales will contribute positively to profitability over a number of years given the long term nature of our business. The Group's solvency position remains strong. With a clear strategic roadmap, a refreshed product suite, and a scalable digital infrastructure, Hansard is well positioned to deliver sustainable growth and long-term value for all stakeholders.

DIVIDENDS

The Board has proposed a final dividend of 2.65p per share, maintaining the total dividend for the year at 4.45p (FY 2024: 4.45p). Subject to shareholder approval at the AGM on 5 November 2025, the dividend will be paid on 13 November 2025 to shareholders on the register at 3 October 2025. The ex-dividend date is 2 October 2025.

HALF-YEARLY RESULTS

The results for the half-year ending 31 December 2025 are expected to be published on 5 March 2026.

For further information:

Tel: +44 (0) 1624 688 000

Email: investor-relations@hansard.com

Camarco

Tel: +44 (0) 7990 653 341

Notes to editors:

·

· The Group offers a range of flexible and tax-efficient investment products within a life assurance policy wrapper, designed to appeal to affluent, international investors.

· The Group utilises a controlled cost distribution model via a network of independent financial advisors, and the retail operations of certain financial institutions who provide access to their clients in more than 170 countries. The Group's distribution model is supported by Hansard OnLine, a multi-language internet platform, and is scalable.

· The principal geographic markets in which the Group currently services contract holders and financial advisors are the

· Hansard

· The Group's objective is to grow by attracting new business and positioning itself to adapt rapidly to market trends and conditions. The scalability and flexibility of the Group's operations allow it to enter or develop new geographic markets and exploit growth opportunities within existing markets often without the need for significant further investment.

Forward-looking statements:

This announcement may contain certain forward-looking statements with respect to certain of

This announcement contains inside information which is disclosed in accordance with the Market Abuse Regime.

Legal Entity Identifier: 213800ZJ9F2EA3Q24K05

Report and Accounts for the year ended 30 June 2025

CHAIRMAN'S STATEMENT

I am pleased to present the Annual Report for the year ended 30 June 2025 ("FY25").

Dr

This year marked the passing of our founder and President, Dr

Financial Performance

The year was one of strong momentum for the Group. New business accelerated, with a 17% increase in APE sales and a 6% rise in PVNBP, reflecting the growing strength of our refreshed proposition and the tentative early success of our international expansion strategy. These results underscore the effectiveness of our strategic investments and the resilience of our business model.

The Group reported an IFRS profit before tax of £1.8m (FY24: £5.3m), with the decline reflecting continued investment in strategic priorities. As we flagged in our results announcement for the first six months of FY25, it will take time for improved sales to fully translate into increased profits. Nonetheless, operational expenses were tightly controlled, and fee income growth helped offset elevated litigation defence costs. Notably, we observed a material reduction in the volume of new litigation writs, and continued insurance recoveries. However, in line with our prudent and disciplined provisioning approach, we have maintained the contingent liability at €23.8m (FY24: €23.8m) to ensure the Group remains appropriately reserved as claims mature and the legal process evolves. A suite of capital management initiatives contributed to a material improvement in solvency, which now stands at 169% prior to the final dividend (2024: 149%), strengthening our ability to sustain shareholder returns over time.

Reflecting the Board's confidence in the Group's financial strength and strategic progress, we have recommended a final dividend of 2.65p per share. This maintains the total dividend for the year at 4.45p-unchanged from FY24. The decision to hold the dividend steady, despite lower IFRS profit, underscores our long-term commitment to capital discipline and sustainable growth. Subject to shareholder approval at the Annual General Meeting, the final dividend of 2.65p per share is scheduled for payment on 13 November 2025. The ex-dividend date will be 2 October, with a record date of 3 October.

Strategic Oversight and Governance

The Board oversaw the successful completion of our enhanced proposition programme, including the launch of new regular premium and investment bond propositions, Ascend and Future Focus, and the continued rollout of Global Select. These initiatives have strengthened our competitive positioning and laid the groundwork for future growth.

We also monitored the Group's expansion into new markets. In

Board Developments

We welcomed

In October 2024, we appointed

We thank

Sustainability and ESG

The Board continues to embed sustainability and ESG into its strategy and operations, reflecting its importance in long-term value creation for the Group.

Business Continuity

Despite the sadness felt at the loss of our founder, the Group continues to operate on a business-as-usual basis. Our leadership team, governance structures, and operational resilience ensure that Hansard remains well positioned to deliver on its strategic objectives and to serve our clients and stakeholders without interruption. Importantly, there has been no change in the Group's strategic direction or ownership following

Outlook

As we look to FY26 and beyond,

Chairman

24 September 2025

CEO REVIEW

Strategic Execution and Market Expansion

FY25 was a year of consolidation and momentum. We embedded the foundations laid in the prior year-enhancing our digital infrastructure, launching a refreshed product suite, expanding our international footprint, and delivering sales growth.

Our new single premium product, Global Select, delivered strong sales in its first full year. Ascend and Future Focus were launched to support regular and flexible premium growth. These products have received positive market feedback and are positioned to drive further momentum in FY26.

Our commitment to product innovation and client outcomes continues to gain external recognition. Recent awards for Ascend and Global Select not only validate the strength of our refreshed proposition but also reflect the growing confidence of distributors and clients in our ability to deliver relevant, high-quality solutions across diverse markets.

In

Operational Efficiency and Technology

We continued to embed and enhance our new policy administration system, implemented in FY24. Now fully operational, the system is undergoing ongoing optimisation to unlock greater automation, scalability, and an improved client experience. These enhancements are expected to deliver long-term cost efficiencies and service benefits.

Strengthening our digital infrastructure remains a strategic priority, and recent industry recognition for client service and fintech innovation reinforces our direction and long-term commitment to delivering a high-quality, technology-enabled experience.

Financial Performance

The Group has delivered stable financial results and positioned itself for long-term, sustainable growth, despite persistent macroeconomic headwinds, including currency fluctuations, inflationary pressures, and interest rate uncertainty. The decline in IFRS profitability reflects our continued investment in strategic priorities and the impact of elevated litigation defence costs. Our solvency position has materially improved, and we continue to manage shareholder assets conservatively to preserve capital and minimise risk.

Financial performance for the year ended 30 June 2025 is summarised as follows:

|

|

2025 |

2024 |

|

|

£m |

£m |

|

New business sales - APE |

12.2 |

10.4 |

|

New business sales - PVNBP |

82.4 |

77.8 |

|

IFRS profit before tax |

1.8 |

5.3 |

|

Underlying IFRS profit |

5.1 |

8.5 |

|

Assets under Administration |

1,129.8 |

1,150.9 |

|

Value of In-Force (regulatory basis) |

103.1 |

110.8 |

FY25 marked a turning point in our growth trajectory, with new business sales rising by 17% on an APE basis, reaching £12.2m (2024: £10.4m), and by 6% on a PVNBP basis, reaching £82.4m (2024: £77.8m)-our strongest annual increase in recent years. This performance was fuelled by the continued success of Global Select, our new proposition launched in late FY24, which helped to deliver a 72.5% uplift in single premium sales. While regular premium sales declined by 10.0%, early signs of recovery are emerging following the launch of Ascend, our award-winning regular premium product, which is gaining traction across key markets and expected to contribute more meaningfully in FY26.

The Group reported an IFRS profit before tax of £1.8m (2024: £5.3m), with underlying IFRS profit (which excludes litigation and non-recurring expenses) of £5.1m (2024: £8.5m). This reduction reflects targeted investment in long-term value drivers, a full year of depreciation from the new system, and elevated litigation defence costs.

Assets under Administration (AuA) stood at £1,129.8m at year-end (2024: £1,150.9m), reflecting net outflows and adverse currency movements, partially offset by strong single premium sales and market gains. The Value of In-Force (VIF) on a regulatory basis was £103.1m (2024: £110.8m), underlining the strength of our long-term revenue-generating capacity.

Fee income remained broadly stable at £48.2m (2024: £48.8m), underpinned by strong equity market performance and resilient contract holder activity. Market conditions improved in the second half of FY25, with global equity markets rebounding to record highs-supporting fee stability. Currency movements and interest rate dynamics continued to influence reported results. The US Dollar depreciated by approximately 8% against Sterling since February, reducing the Sterling value of our USD-denominated income.

Administrative and other expenses rose to £36.7m (2024: £33.3m), driven by investment in capacity and capability to support future growth, and defending legacy litigation. Origination costs decreased to £15.0m (2024: £16.1m), with lower acquisition costs and stable amortisation of deferred expenses.

Cash flows before dividends were negative £2.9m (2024: inflows of £3.0m), primarily due to a £3.8m investment into a corporate bond, and investment in new business acquisition and IT infrastructure. Despite this, we maintained our dividend at 4.45p per share, reflecting our confidence in the Group's capital strength and long-term prospects.

The Group remains well capitalised, supported by a series of capital management initiatives implemented during the year that have materially strengthened our solvency position. Under risk-based capital methodologies, total Group Free Assets in excess of the Solvency Capital Requirement stood at £45.6m (2024: £39.4m), representing a coverage ratio of 169% (2024: 149%).

Shareholder assets continue to be managed conservatively, held across a diversified portfolio of deposit institutions, investment-grade corporate bonds, and highly rated money market liquidity funds. This prudent investment strategy has minimised market risk and underpinned the Group's financial stability and resilience over recent years.

Litigation

We are proactively managing legacy litigation linked to Hansard Europe dac, with a focus on reducing exposure, securing insurance recoveries, and protecting the Group's reputation and capital position. At 30 June the net cumulative exposure was €23.8m (£20.4m), and the Group noted a material reduction in the volume of new writs during the year and recorded £0.4m in insurance recoveries. While resolution timelines vary by jurisdiction, our legal strategy remains robust, and we expect continued progress in FY26 as claims mature and recoveries advance.

Sustainability and ESG Progress

We also advanced our ESG agenda, expanding our community engagement efforts, and embedding sustainability into our operations. We achieved a 9% reduction in Scope 1 and 2 emissions, expanded our community engagement efforts with over 500 hours of volunteering, and embedded sustainability into our operations and governance frameworks. These initiatives reflect our belief that long-term success must be underpinned by responsible business practices.

People and Culture

Our people remain the key driver of our success. On behalf of the Board, I would like to express our sincere appreciation to all colleagues across the Group. Their commitment to our clients, adaptability in the face of change, and shared belief in our long-term vision have been instrumental in navigating a complex environment and positioning the business for future success.

The passing of our founder and President, Dr

Looking Ahead

FY26 marks a pivotal year in our strategic journey. Our refreshed strategy is guided by three imperatives: improving our business, growing our footprint, and future-proofing our business model.

Our FY26 priorities are:

· Improve: Strengthen our proposition and continue to focus on our customer service.

· Grow: Launch our Japanese proposition and continue to work with new distributors in

· Future-proof: Optimise our operating model and manage legacy litigation.

While short-term pressures on profitability persist, our solvency remains strong, our strategy is clear, and our people are energised. We remain focused on delivering sustainable value for all stakeholders.

Group Chief Executive Officer

24 September 2025

OUR BUSINESS MODEL AND STRATEGY

Strategic Context and Vision

At Hansard, our mission is to empower clients to achieve lasting financial success while cultivating trusted relationships with quality distributors.

Our vision is to deliver competitive and innovative financial solutions to clients worldwide leveraging the expertise of high-quality distributors - anchored in trust, integrity, respect, quality, and innovation.

FY25 marked a pivotal year in our strategic journey. With new propositions launched, international expansion underway, and continued investment in digital infrastructure, we have laid the groundwork for sustainable growth. Our strategy is clear: to improve our business, grow our footprint, and future-proof our business model.

This strategy is underpinned by three imperatives:

· Improve: We are committed to enhancing client outcomes by recruiting, training, and retaining quality people; delivering excellent customer service; and strengthening our proposition through distributor feedback and market insight.

· Grow: We are focused on organic expansion, including our re-entry into the Japanese market and deepening distributor relationships. We continue to develop bespoke distributor partnerships that support scalable, long-term growth.

· Future-proof: We are committed to embracing innovation and digital transformation to elevate client experiences, drive operational efficiency, and ensure resilience in a dynamic regulatory and economic environment.

These imperatives are not abstract ambitions. They are embedded in our day-to-day operations and reflected in our strategic initiatives for FY26, including enhancements to our product and fund range, and drive excellent customer service standards.

Our people remain central to our success. By fostering a culture of empowerment, accountability, and continuous improvement, we are building a business that is not only fit for the future but also aligned with the values that have defined Hansard for nearly four decades.

Our strategic commitment to sustainability is not only reflected in our ESG initiatives but also embedded in our enterprise risk management and long-term planning frameworks. Climate-related risks and opportunities are actively assessed across our strategic pillars-Improve, Grow, and Future-proof-and are integrated into our governance, investment, and operational decisions.

For a more detailed overview of how these considerations are embedded into our risk management, scenario modelling, and strategic resilience planning, please refer to our TCFD-aligned disclosures in the Sustainability and ESG Integration section. These disclosures outline our approach to governance, strategy, risk management, and metrics and targets in relation to climate-related financial risks and opportunities.

Our Business Model

Hansard is a specialist provider of long-term savings and investment solutions, operating through a network of regulated entities across the

We serve a diverse client base of affluent international investors, institutions, and wealth-management groups, administering assets in excess of £1 billion across nearly 40,000 client accounts. Our products are exclusively distributed through IFAs and the retail operations of financial institutions, with local language support provided by our Regional Sales Managers and our award-winning Hansard OnLine platform.

Our operations are structured to ensure regulatory compliance, operational efficiency, and strategic agility. Each of our regulated entities plays a distinct role:

·

· Hansard Worldwide (The

· Hansard

We do not offer investment advice, and our products carry no investment guarantees, ensuring that contract holders bear the investment risk. This model allows us to maintain a low-risk balance sheet and minimise capital strain, while offering clients access to a wide range of investment assets tailored to their needs.

Our business model is designed to scale efficiently, adapt to regulatory change, and support strategic growth initiatives. In FY26, this includes the launch of our Japanese proposition, enhancements to our product and fund ranges, and the raising of excellent customer service standards.

Executing Our Strategy

Our strategy is built around three imperatives-Improve, Grow, and Future-proof-which guide our decision-making and operational priorities across the Group. These pillars are not static; they evolve in response to market dynamics, client expectations, and regulatory developments. In FY26, we are executing this strategy through a focused set of initiatives that reflect our ambition to deliver sustainable growth and long-term value.

1. Improve

We are committed to enhancing client outcomes and operational excellence by:

· Delivering excellent customer service:

· Strengthening our proposition: We are refreshing our back-book fund range and introducing new product features such as segmentation, multiple beneficiaries, and alternative charging structures.

· Listening to distributors: Feedback loops are embedded into our product development and service design processes, ensuring our offerings remain relevant and competitive.

2. Grow

We are expanding our footprint and deepening relationships in key markets:

·

·

· Product innovation: We are developing innovative new products together with our distributors.

3. Future-proof

We are investing in technology, governance, and resilience to ensure long-term sustainability:

· Digital transformation: We continue to enhance our policy administration system and are completing the decommissioning of legacy systems.

· Operational efficiency: Projects such as e-invoicing, re-engineered reconciliations, and operational optimisation are designed to streamline processes and reduce cost-to-serve.

· Risk and compliance: We are implementing a new risk management platform and strengthening our regulatory reporting capabilities, including FATCA/CRS compliance.

· Litigation management: We are proactively managing legacy litigation with a focus on reducing exposure, securing insurance recoveries, and protecting the Group's reputation and capital position.

Together, these initiatives reflect our ambition to deliver sustainable growth, enhance client outcomes, and build a resilient, future-ready business.

Our strategy is supported by a disciplined approach to capital allocation, a strong solvency position, and a culture that values innovation, accountability, and client-centricity.

Our Products

Hansard's product suite is designed to meet the long-term savings and investment needs of international clients through secure, flexible, and transparent life assurance wrappers. Our contracts are unit-linked, offering access to a broad range of investment assets, and are available on a regular, single, or flexible premium basis.

We do not offer investment advice, and our products do not include financial guarantees or options. This ensures that contract holders bear the investment risk, while the Group minimises capital strain and maintains a low-risk balance sheet.

Our products are distributed exclusively through IFAs and the retail operations of financial institutions. We support these partners with multilingual digital tools, including Hansard OnLine and Online Accounts, which enable real-time policy management and fund performance tracking.

In FY24, we launched Global Select, a single premium product that has delivered strong uptake and is now being enhanced with segmentation and additional charging options.

We also introduced Ascend and Future Focus in FY25, designed to support regular and flexible premium growth. These products are being further refined to include features such as multiple beneficiaries and lower minimum premiums. Each product is designed to meet specific client profiles-from Global Select's appeal to lump-sum investors, to Ascend and Future Focus supporting regular and flexible premium savers.

Looking ahead, we are preparing to launch two new regulated products in

· Global Access - a regular premium savings product tailored to the Japanese domestic market.

· Upstream - a flexible premium investment bond designed to meet the evolving needs of Japanese investors.

These launches mark a significant milestone in our international expansion strategy and reflect our commitment to delivering competitive, relevant solutions in high-potential markets.

We are also developing new innovative products and extending our fund range to ensure continued relevance and competitiveness.

These enhancements are informed by distributor feedback and market analysis and are aligned with our commitment to delivering a standout value proposition.

Our commitment to product excellence has been recognised through multiple industry awards, including recent accolades for Best International Savings Plan for Ascend and Highly Commended International Portfolio Bond Product for Global Select. These achievements reflect our ongoing investment in product enhancement and client outcomes.

Our product strategy is focused on simplicity, transparency, and adaptability-enabling clients to align investments with their goals through secure, scalable structures and features like flexible contributions, clear fees, and intuitive digital tools. Together, these ensure a compelling offering that delivers strong value for money and stands out in a competitive international market.

Revenue Model

Hansard's revenue model is built on the administration of long-term savings and investment contracts. Our primary source of income is the fees earned from managing these contracts, which are largely fixed in nature and resilient to market volatility. This provides a stable and predictable income stream that supports operational resilience and long-term planning.

Approximately one-third of our revenue is linked to the value of assets under administration (AuA), which stood at £1.13 billion as at 30 June 2025. This component of income benefits from favourable market conditions and strong single premium inflows, such as those generated by Global Select.

The Group's revenue model is exposed to macroeconomic variables, particularly currency movements and interest rates. Approximately three-quarters of premiums are received in US Dollars-serving as a proxy for income exposure-while most expenses are settled in Sterling. This creates a structural exposure to USD/GBP exchange rate fluctuations. Although the Group does not currently hedge foreign currency cash flows, excess foreign currency is regularly converted to Sterling to manage volatility. Based on current business volumes, a 5% movement in the USD/GBP exchange rate typically affects annual fee income by approximately £1.9m.

Our prudent approach to treasury management ensures that shareholder assets are conservatively invested across a diversified portfolio of deposit institutions, investment-grade corporate bonds, and highly rated liquidity funds. This strategy minimises market risk and underpins the Group's financial stability.

Our fee-based model enables us to:

· Fund ongoing investment in digital infrastructure, product development, and service enhancements.

· Remunerate our global distribution network of independent financial advisers.

· Maintain a stable dividend policy, reflecting the Board's confidence in the Group's capital strength and strategic direction.

· Absorb the costs of strategic initiatives and litigation defence while preserving solvency and liquidity.

We continue to optimise our cost base through operational efficiency projects, including process re-engineering and automation. These initiatives are designed to reduce the Group's cost-to-serve and enhance scalability as we grow our international footprint.

As we execute our FY26 business plan, we remain focused on balancing investment in growth with disciplined cost control and capital stewardship, ensuring that our revenue model continues to support sustainable value creation for all stakeholders.

Managing Risk

Hansard operates in a complex and evolving global environment, where macroeconomic volatility, regulatory change, and geopolitical uncertainty present both challenges and opportunities. Our approach to risk management is grounded in prudence, transparency, and continuous improvement-ensuring that we protect our stakeholders while enabling sustainable growth.

We maintain a robust, low-risk balance sheet and a conservative investment strategy. Our products carry no investment guarantees or options, which limits capital strain and market exposure. This model allows us to focus on long-term value creation while preserving financial flexibility.

Our enterprise risk management ("ERM") Framework is designed to identify, assess, and mitigate risks across all areas of the business. The Framework is embedded in our governance structures and aligned with international regulatory standards with continued commitment to improving risk visibility, responsiveness, and integration across the Group.

Key areas of focus include:

· Operational resilience: We are strengthening our systems and controls to ensure continuity of service and data integrity, particularly as we scale our digital infrastructure and decommission legacy systems.

· Regulatory compliance: We continue to work closely with regulators across all jurisdictions, adapting to evolving supervisory expectations and embedding regulatory change into our strategy, policy, and culture.

· Litigation management: We are proactively managing legacy litigation linked to Hansard Europe dac, with a focus on reducing exposure, securing insurance recoveries, and protecting the Group's reputation and capital position.

· Cybersecurity: We are investing in advanced detection and defence capabilities to safeguard client data and maintain trust in our digital platforms.

Our risk culture is supported by clear accountability, regular training, and open communication. We believe that effective risk management is not only a regulatory requirement but a strategic enabler-allowing us to innovate with confidence, serve clients with integrity, and deliver long-term value to shareholders.

Digital Innovation and Client Experience

Digital innovation is central to Hansard's strategy to improve client outcomes, enhance operational efficiency, and future-proof the business. Our technology platforms are continually being re-designed to support scalable growth, enable seamless adviser and client interactions, and deliver a consistently high standard of service across jurisdictions.

Our flagship platform, Hansard OnLine, is used daily by IFAs around the world. It provides real-time access to policy information, transaction tools, and fund performance data in multiple languages. Complementing this, our Online Accounts platform empowers clients to manage their policies securely, 24/7, from any device, supporting transparency, engagement, and long-term retention.

In FY25, we completed the implementation of a new policy administration system, which is now fully operational. This system forms the backbone of our digital infrastructure and is being continuously enhanced to unlock automation, improve scalability, and reduce manual processing. These improvements are expected to yield cost savings and service benefits over time.

In FY26, we are advancing several digital initiatives to further elevate our technology advantage:

· New APIs to improve onboarding and servicing efficiency.

· E-invoicing and automated reconciliations to enhance financial operations and reduce turnaround times.

· Legacy system decommissioning to streamline architecture and reduce operational risk.

Our commitment to digital excellence has been recognised through multiple industry awards in recent years, including accolades for Excellence in Client Service (

As we continue to innovate, we remain guided by our values of trust, quality, and innovation-ensuring that every digital enhancement contributes to a more responsive, secure, and client-centric business.

Regulatory Engagement

Hansard operates in a highly regulated, multi-jurisdictional environment. We view regulatory engagement not as a compliance obligation alone, but as a strategic enabler-supporting market access, client confidence, and long-term sustainability.

Our principal operating entities are authorised and supervised by regulators in the

In the

We also worked closely with the Insurance Commission of The

Throughout FY25, we worked closely with the Japan

We seek iterative improvements to our compliance infrastructure to ensure that:

· Our compliance systems and controls remain robust and effective on a continuing basis. Our capacity to manage regulatory change on a timely and effective basis is embedded into our strategy, our policies, and our culture.

· We remain committed to upholding the highest standards of integrity, transparency, and accountability. Our regulatory engagement strategy is designed to protect clients, support innovation, and ensure that Hansard remains a trusted partner in every market in which we operate.

Sustainability and ESG Integration

At Hansard, sustainability is not a standalone initiative-it is embedded in our strategy to improve, grow, and future-proof the business. We recognise that long-term value creation depends on our ability to operate responsibly, minimise our environmental impact, and contribute positively to the communities in which we operate.

Our ESG approach is structured around three pillars:

· Environmental Responsibility: We are committed to reducing our carbon footprint and improving environmental performance across our operations. In FY25, we achieved a 9% reduction in Scope 1 and 2 emissions, supported by initiatives such as transitioning to renewable energy tariffs, reducing business travel, and investing in verified carbon offset programmes. We continue to enhance our data collection and reporting capabilities, with the aim of setting absolute reduction targets across all material emission categories.

· Social Impact: We foster a culture of inclusion, wellbeing, and community engagement. Our Wellbeing and Green Teams led over 500 hours of volunteering and sustainability-focused activities during the year, including biodiversity projects, youth education programmes, and support for local charities. We also expanded our employee development initiatives, with a focus on resilience, leadership, and service excellence.

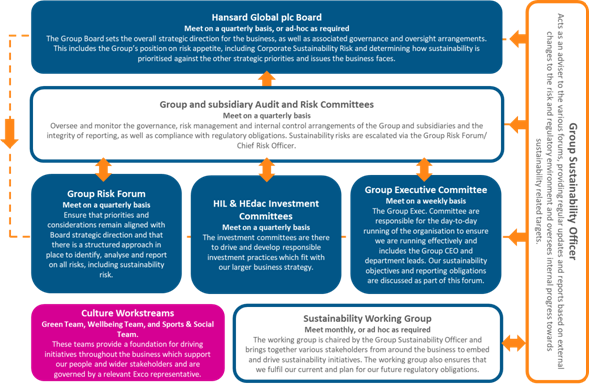

· Governance and Risk Management: ESG risks and opportunities are integrated into our ERM Framework and overseen by the Board and Executive Committee. ESG is a standing agenda item at Board meetings, and our governance structures ensure clear accountability for sustainability performance. We continue to align our disclosures with the TCFD framework and are preparing for broader sustainability reporting requirements.

Looking ahead, we will continue to refine our ESG strategy, with a focus on:

· Embedding sustainability into product development and investment governance.

· Enhancing Scope 3 emissions tracking, particularly across our value chain.

· Supporting clients and advisers with ESG-related fund insights and tools.

· Aligning our practices with emerging regulatory standards and stakeholder expectations.

Our ambition is to be recognised not only for the quality of our products and services, but also for the integrity and responsibility with which we operate.

KEY PERFORMANCE INDICATORS

The Group's senior management team monitors a wide range of Key Performance Indicators, both financial and non-financial, that are designed to ensure that performance against targets and expectations across significant areas of activity are monitored and variances explained.

The following is a summary of the key indicators that were monitored during FY25.

|

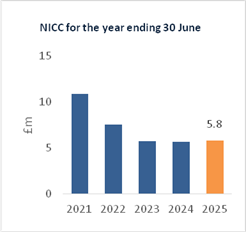

New Business - The Group's internal indicator of calculating new business production, Net Issued Compensation Credit ("NICC") reflects the amount of base commission payable to intermediaries, excluding override commission. Incentive arrangements for intermediaries and the Group's Regional Sales Managers incorporate targets based on NICC (weighted where appropriate). New business levels are reported daily and monitored weekly against target levels. Net Issued Compensation Credit was £5.8m for the year, up £0.2m on 2024, reflective of higher new business levels. |

|

|

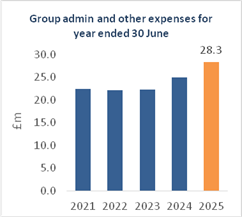

Administrative Expenses (excl. litigation and non-recurring items) - The Group maintains a rigorous focus on expense levels and the value gained from such expenditure. The objective is to develop processes to restrain increases in administrative expenses to the rates of inflation assumed in the charging structure of the Group's policies.

The Group's administrative and other expenses for the year (excl. litigation and non-recurring items) were £28.3m compared to £25.0m in 2024. Further detail is contained in the section on Administrative and other expenses on page 19. |

|

|

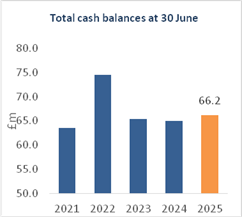

Cash - Bank balances and significant movements on balances are reported monthly. The Group's cash and deposits at the balance sheet date were £66.2m (2024: £65.0m). Movements are reflective of cash earned from new and existing business, commissions and expenses paid, investments in new systems, the level of inflight transactions, and the dividends paid to shareholders. |

|

|

Operational Resilience - Maintenance of continual access to data is critical to the Group's operations. This has been achieved throughout the year through a robust infrastructure. The Group is pro-active in its consideration of threats to data, data security and data integrity. Business continuity and penetration testing is carried out regularly by internal and external parties. Operational Resilience is further evidenced by ongoing remote working as a normal business practice. |

|

|

Risk profile - The factors impacting on the Group's risk profile are kept under continuous review. Senior management review actual and emerging risks at least monthly. The principal risks faced by the Group are summarised in the Principal Risks section. |

|

|

Solvency - The Solvency Capital Requirement ("SCR") of the Group and its subsidiaries is monitored frequently and reported to the Board. The SCR as at 30 June 2025 is reported in Other Information on page 153. |

|

business AND FINANCIAL REVIEW

NEW BUSINESS PERFORMANCE FOR THE YEAR ENDED 30 JUNE 2025

The Group remains focused on distributing both regular and single premium products across a broad range of international markets, achieving well-diversified and resilient new business growth.

New business performance for the year is summarised in the table below:

|

|

2025 |

2024 |

% |

|

Basis |

£m |

£m |

change |

|

Annualised Premium Equivalent ("APE") |

12.2 |

10.4 |

17.3% |

|

Present Value of New Business Premiums ("PVNBP") |

82.4 |

77.8 |

5.9% |

Annual Premium Equivalent ("APE")

New business for FY25 totalled £12.2m (2024: £10.4m) on an APE basis, representing a 17.3% increase on the prior year. This growth was primarily driven by the continued success of Global Select, our new proposition launched in late FY24, which helped to deliver a 72.5% uplift in single premium sales. While regular premium sales declined by 10.0%, early signs of recovery are emerging following the launch of our award-winning regular premium product, Ascend, which is gaining traction across key markets.

New business flows on the APE basis for the Group are as follows:

|

|

2025 |

2024 |

% |

|

APE by product type |

£m |

£m |

change |

|

Regular premium |

6.2 |

6.9 |

(10.0%) |

|

Single premium |

6.0 |

3.5 |

72.5% |

|

Total |

12.2 |

10.4 |

17.3% |

Present Value of New Business Premiums ("PVNBP")

New business for FY25 totalled £82.4m (2024: £77.8m) on a PVNBP basis, representing a 5.9% increase on the prior year.

New business flows on the PVNBP basis for the Group are as follows:

|

|

2025 |

2024 |

% |

|

PVNBP by product type |

£m |

£m |

change |

|

Regular premium |

27.9 |

44.2 |

(36.9%) |

|

Single premium |

54.5 |

33.6 |

62.2% |

|

Total |

82.4 |

77.8 |

5.9% |

|

|

|

|

|

|

|

2025 |

2024 |

% |

|

PVNBP by region |

£m |

£m |

change |

|

|

32.9 |

32.4 |

1.5% |

|

Rest of World |

16.2 |

16.4 |

(1.4%) |

|

|

28.1 |

24.3 |

15.7% |

|

Far East |

5.2 |

4.7 |

11.0% |

|

Total |

82.4 |

77.8 |

5.9% |

The launch of our new single premium proposition, Global Select, received positive market feedback and drove a significant uplift in single premium business during the year, a trend we expect to continue into FY26 and beyond. In parallel, the upcoming launch of new regular premium products through our distribution agreement with Guardian in

Activity levels across our distribution network remain high, with several new relationships already generating business. Our sales team is focused on deepening engagement and driving product innovation-developing new offerings for priority markets, refining existing products, and advancing system improvements that elevate our service proposition.

This momentum in new business volumes-particularly in single premium flows-demonstrates the effectiveness of our product innovation and distributor engagement strategies. With new launches planned and a strengthened regular premium offering, we are confident in our ability to sustain this growth into FY26 and beyond.

Premium currency composition remained broadly stable year-on-year, with US Dollars continuing to represent the primary denomination:

|

|

2025 |

2024 |

|

Currency denominations (as a percentage of PVNBP) |

% |

% |

|

US dollar |

78 |

85 |

|

Sterling |

16 |

10 |

|

Euro |

6 |

4 |

|

Other |

- |

1 |

|

|

100 |

100 |

Presentation of financial results

The Group's business is inherently long term, and this is reflected in the way new business flows impact reported earnings under

Results for the year

The summary below outlines the key components of the Group's financial results for the year.

IFRS profit before tax for the year was £1.8m, down from £5.3m in FY24. While fee income and investment returns increased, these gains were offset by higher administrative expenses, reflecting continued investment in strategic initiatives and enhanced legacy litigation defence.

Operating profit before litigation and non-recurring items was £5.1m, compared to £8.5m in FY24, highlighting the impact of elevated cost pressures and the amortisation of prior investments.

Abridged consolidated income statement

The consolidated statement of comprehensive income, prepared in accordance with IFRS, presents the Group's financial results for the year. However, due to the nature of its presentation, it includes certain features that may obscure the underlying performance of the Group's own activities. In particular:

· Investment gains attributable to contract holder assets totalled £27.1m (2024: £114.4m). These assets are selected by the contract holder or their authorised intermediary, and the associated investment risk is borne by the contract holder. Corresponding changes in the value of these assets are reflected within 'Change in provisions for investment contract liabilities', resulting in no net impact on IFRS profit.

· Fund management fees of £5.1m (2024: £5.1m) were collected and passed through to third parties with a relationship to the underlying contracts. Under IFRS, these are reported on a gross basis within both income and expenses. Adjusting for this, fees and commissions attributable to Group activities reduce from £48.2m to £43.1m, and administrative and other expenses reduce from £36.7m to £31.6m, as shown in the abridged income statement below.

The abridged non-GAAP consolidated income statement below presents the Group's underlying financial performance, adjusted to exclude items outlined above for a clearer view of core operating activity.

|

|

2025 |

2024 |

|

|

£m |

£m |

|

Fees and commissions attributable to Group activities |

43.1 |

43.7 |

|

Investment and other income |

5.3 |

5.9 |

|

|

48.4 |

49.6 |

|

Origination costs |

(15.0) |

(16.1) |

|

Administrative and other expenses attributable to the Group, excluding depreciation and amortisation and before litigation and non-recurring expense items |

(26.2) |

(24.0) |

|

Depreciation and amortisation |

(2.1) |

(1.0) |

|

Operating profit for the year before litigation and non-recurring items |

5.1 |

8.5 |

|

Litigation and non-recurring expense items |

(3.3) |

(3.2) |

|

Profit for the year before taxation |

1.8 |

5.3 |

|

Taxation |

- |

(0.1) |

|

Profit for the year after taxation |

1.8 |

5.2 |

Fees and commissions

Fees and commissions attributable to Group activities totalled £43.1m for FY25, a decrease of 1.4% compared to £43.7m in FY24.

Contract fee income amounted to £29.2m, down £1.4m from the prior year's £30.6m. This includes both the amortised portion of up-front income deferred under IFRS and contract-servicing charges. Within this:

· Amortisation of deferred income in

· Transactional charges related to policyholder activity fell to £12.5m.

· Hansard

Fund management fees and commissions receivable from third parties totalled £13.9m, up from £13.1m in 2024. These are directly linked to the value of assets under administration and are influenced by market performance, currency fluctuations, and valuation assumptions.

A summary of fees and commissions is set out below:

|

|

2025 |

2024 |

|

|

£m |

£m |

|

Contract fee income |

29.2 |

30.6 |

|

Fund management fees accruing to the Group |

8.8 |

8.3 |

|

Commissions receivable |

5.1 |

4.8 |

|

|

43.1 |

43.7 |

Contract fee income includes £15.8m (2024: £17.4m) relating to the amortisation of fees deferred in prior years, as detailed in the analysis below:

|

|

2025 |

2024 |

|

|

£m |

£m |

|

Amortisation of deferred income |

15.8 |

17.4 |

|

Income earned during the year |

13.4 |

13.2 |

|

Contract fee income |

29.2 |

30.6 |

Investment and other income

Investment and other income decreased to £5.0m as a result of the reclassification of £0.3m (2024: £0.7m) of other income as contract fee income in the current year. Underlying bank interest income rose by £0.3m, reflecting the Group's proactive treasury management and the benefit of higher interest rates during the year.

|

|

2025 |

2024 |

|

|

£m |

£m |

|

Bank interest and other income receivable |

5.0 |

5.5 |

|

Foreign exchange profits on revaluation of net operating assets |

0.3 |

0.4 |

|

|

5.3 |

5.9 |

Origination costs

Under IFRS, new business commissions and directly attributable incremental costs incurred at contract inception are deferred and amortised over the expected life of each contract, aligning expenses with the longer-term income streams they generate. Typical amortisation periods range from 8 to 15 years, depending on the product type. Other new business costs-such as sales employee staff salaries-are expensed as incurred.

Origination costs incurred in FY25 totalled £9.2m, a decrease of £1.1m compared to £10.3m in FY24. This reduction reflects a decline in the amortisation of previously deferred costs.

|

|

2025 |

2024 |

|

|

£m |

£m |

|

Origination costs - deferred to match future income streams |

7.4 |

8.2 |

|

Origination costs - expensed as incurred |

1.8 |

2.1 |

|

Investment in new business in year |

9.2 |

10.3 |

|

Amortisation of deferred origination costs net of new deferrals |

5.8 |

5.8 |

|

|

15.0 |

16.1 |

In addition, £13.2m (2024: £13.9m) was expensed to match contract fee income earned during the year from contracts issued in prior periods.

Summarised origination costs for the year were:

|

|

2025 |

2024 |

|

|

£m |

£m |

|

Amortisation of deferred origination costs |

13.2 |

13.9 |

|

Other origination costs incurred during the year |

1.8 |

2.2 |

|

|

15.0 |

16.1 |

Administrative and other expenses

The Group continues to manage its expense base with discipline, balancing cost control with targeted investment to support strategic initiatives and new business growth.

A detailed breakdown of administrative and other expenses is provided in notes 8 and 9 to the consolidated financial statements. The summary below focuses on expenses attributable to the Group's own activities, excluding third-party fund management fees of £5.1m (2024: £5.1m), which are collected and passed through to external parties associated with underlying contracts.

|

|

2025 |

2024 |

|

|

£m |

£m |

|

Salaries and other employment costs |

12.3 |

11.3 |

|

Other administrative expenses |

9.8 |

7.8 |

|

Professional fees, including audit |

3.6 |

3.2 |

|

Recurring administrative and other expenses |

25.7 |

22.3 |

|

Growth investment spend |

2.6 |

2.7 |

|

Administrative and other expenses, excl. litigation and non-recurring expense items |

28.3 |

25.0 |

|

Litigation defence and settlement costs |

2.8 |

2.5 |

|

Provision for doubtful debts |

0.5 |

0.7 |

|

Total administrative and other expenses |

31.6 |

28.2 |

Salaries and other employment costs increased by £1.0m (9.0%) to £12.3m in FY25. Although average Group headcount declined slightly to 180 (2024: 182), the increase reflects that in FY24 there were £1.3m of capitalised salary costs for the implementation of the new policy administration system. In addition, temporary resourcing was added to strengthen the Client Services team during the post-migration period.

Other administrative expenses increased by £2.0m to £9.8m, with the first full year amortisation charge of the policy administration system of £1.2m, with further strategic development expenditure of £1.0m to support the policy administration system. These costs were offset by efficiency savings in underlying administrative costs, despite ongoing inflationary pressures.

Professional fees, including audit, rose by £0.4m to £3.6m. This includes:

· £0.8m paid to the Group's auditor (2024: £0.9m),

· £0.6m (2024: £0.6m) for administration, custody, dealing, and other charges under the Group's investment processing outsourcing arrangements,

· £0.1m (2024: £0.2m) in recruitment costs, and

· £0.2m (2024: £0.2m) for investor relations activities.

Growth investment spend reduced to £2.6m, reflecting internal and external costs associated with strategic initiatives aimed at leveraging the capabilities of the new policy administration system. Following its implementation, smaller incremental developments are no longer capitalised and are instead recognised as incurred. The total also includes expenditure related to the development and delivery of the Group's Japanese proposition and other new product initiatives.

Litigation defence and settlement costs represent expenses incurred in defending Hansard Europe against legal claims, net of insurance recoveries. Further detail is provided in note 26 to the consolidated financial statements. During the year, legal cost recoveries from insurers totalled £0.4m (2024: £0.7m). A litigation provision of £0.3m was recognised in FY25, bringing the total provision at 30 June 2025 to £0.7m (2024: £0.5m).

Provision for doubtful debts relates to the full impairment of fees and other balances deemed irrecoverable, primarily from legacy Hansard Europe funds currently undergoing liquidation proceedings.

Cash Flow ANALYSIS

The Group generated an operational cash surplus of £4.6m in FY25, down from £10.9m in FY24, reflecting increased operational expenditure to support strategic initiatives and position the business for future growth.

As is typical for our business model, writing new business-particularly regular premium contracts-creates a short-term cash strain due to upfront commission and acquisition costs. These are offset over time by annual management charges, which generate a positive return as contract holder assets accumulate.

The Group's strong liquidity position enables it to fund new business growth where required. The Group aims to achieve sufficient new business growth so that assets under administration increase over time, and recurring fee income becomes sufficient to support both new business acquisition and dividend payments on a self-sustaining basis. During FY25, the Group invested £1.0m (2024: £3.9m) in further enhancements to its policy administration system and computer equipment. These costs were capitalised as detailed in note 13 to the consolidated financial statements.

Net cash outflows before dividends were £2.9m (2024: inflows of £3.0m), primarily due to the completion of the system replacement project and a further £3.8m investment in a bond portfolio.

Despite these investments, Group cash and deposits increased to £66.2m as at 30 June 2025 (2024: £65.4m), primarily due to the increase in amounts due to contract holders.

The following non-GAAP tables summarise the Group's own cash flows in the year:

|

|

2025 |

2024 |

|

|

£m |

£m |

|

Net cash surplus from operating activities |

4.6 |

10.9 |

|

Interest received |

4.7 |

4.2 |

|

Net cash inflow from operations |

9.3 |

15.1 |

|

Net cash investment in new business |

(7.3) |

(8.1) |

|

Purchase of property and computer equipment |

(1.0) |

(3.9) |

|

Net cash investment in bond portfolio |

(3.8) |

- |

|

Corporation tax paid |

(0.1) |

(0.1) |

|

Net cash (outflow) / inflow before dividends |

(2.9) |

3.0 |

|

Dividends paid |

(6.1) |

(6.1) |

|

Net cash outflow after dividends |

(9.0) |

(3.1) |

|

|

|

|

|

|

|

|

2025 |

2024 |

|

|

|

|

£m |

£m |

|

|

|

Net cash outflow after dividends |

(9.0) |

(3.1) |

||

|

Increase in amounts due to contract holders |

9.2 |

2.7 |

||

|

Net Group cash movements |

0.2 |

(8.1) |

||

|

Group cash and deposits - opening position |

65.0 |

65.4 |

||

|

Effect of exchange rate movements |

1.0 |

- |

||

|

Group cash and deposits - closing position |

66.2 |

65.4 |

||

The below table reconciles the key lines for this year in the above non-GAAP cash flow to the key lines in the consolidated cash flow shown on page 108.

|

|

Non-GAAP Cash Flow |

Consolidated Cash Flow Statement |

|

|

£m |

£m |

|

Net cash flow from operations before tax |

9.3 |

14.0 |

|

Adjust for net movement in policyholder financial assets and liabilities |

- |

(1.7) |

|

|

9.3 |

12.3 |

|

|

|

|

|

Purchase of property and computer equipment (tangible and intangible) |

(1.0) |

(1.0) |

|

|

|

|

|

Corporation tax paid |

(0.1) |

(0.1) |

|

|

|

|

|

Dividends paid |

(6.1) |

(6.1) |

|

|

|

|

|

Net cash investment in business |

(7.3) |

- |

|

Cashflows from investing activities |

(3.8) |

(3.9) |

|

Increase in amounts due to contract holders |

9.2 |

- |

|

Net movement in assets and liabilities relating to contract holders |

- |

(1.0) |

|

|

(1.9) |

(4.9) |

|

|

|

|

|

Net Group cash movements |

0.2 |

0.2 |

Group bank deposits and money market funds

The Group maintains its liquid assets in highly rated money market funds and across a diversified range of deposit institutions to mitigate counterparty risk. As at 30 June 2025, deposits totalling £14.7m (2024: £17.1m) had original maturity dates exceeding three months and are therefore excluded from the definition of "cash and cash equivalents" under IFRS. These are instead classified as 'Deposits and money market funds' in the consolidated balance sheet.

|

|

2025 |

2024 |

|

|

£m |

£m |

|

Money market funds and immediately available cash |

50.9 |

47.3 |

|

Short-term deposits with credit institutions |

0.6 |

0.6 |

|

Cash and cash equivalents under IFRS |

51.5 |

47.9 |

|

Deposits and money market funds |

14.7 |

17.1 |

|

Group cash and deposits |

66.2 |

65.0 |

Abridged consolidated balance sheet

The consolidated balance sheet on page 107, prepared in accordance with IFRS, reflects the Group's financial position as at 30 June 2025. Due to its presentation format, it includes both the financial assets held to back the Group's liabilities to contract holders and the corresponding net liability of £1,129.8m (2024: £1,150.9m). In addition, the portion of the Group's capital held in bank deposits is reported within "cash and cash equivalents" based on original maturity terms, as outlined in the preceding section.

To provide a clearer view of the Group's own capital position, the abridged consolidated balance sheet below adjusts for these presentation differences:

|

|

2025 |

2024 |

|

|

£m |

£m |

|

Assets |

|

|

|

Deferred origination costs |

106.3 |

112.1 |

|

Other assets |

47.7 |

38.7 |

|

Bank deposits and money market funds |

66.2 |

65.0 |

|

|

220.2 |

215.8 |

|

Liabilities |

|

|

|

Deferred income |

137.5 |

140.2 |

|

Other payables |

66.2 |

54.7 |

|

|

203.7 |

195.0 |

|

Net assets |

16.5 |

20.8 |

|

Shareholders' equity |

|

|

|

Share capital and reserves |

16.5 |

20.8 |

Other assets include intangible assets, property, plant and equipment, and other receivables.

Other payables comprise amounts due to investment contract holders and other liabilities.

Deferred origination costs

Deferred origination costs represent acquisition expenses that are recoverable from future income streams generated by contracts issued during the year. These costs are amortised on a straight-line basis over the expected life of each contract.

The table below summarises the movement in deferred origination costs over the financial year.

|

|

2025 |

2024 |

|

Carrying value |

£m |

£m |

|

At beginning of financial year |

112.1 |

117.8 |

|

Origination costs deferred during the year |

7.4 |

8.2 |

|

Origination costs amortised during the year |

(13.2) |

(13.9) |

|

|

106.3 |

112.1 |

Deferred income

Deferred income reflects initial fees received on new business that are recognised in the income statement over the life of the contract, in line with the services provided. This treatment mirrors that of deferred origination costs.

The proportion of income deferred each year depends on the mix and volume of new business. With regular premium business, initial fees are typically received over the early years of the contract rather than upfront, as is common with single premium contracts.

Most of the initial fees recognised in FY25 relate to contracts issued in prior years, highlighting the cash-generative nature of the business. Regular premium contracts issued in FY25 are expected to generate most of their initial fees over the next 18 months.

The table below summarises the movement in deferred income over the financial year.

|

|

2025 |

2024 |

|

Carrying value |

£m |

£m |

|

At beginning of financial year |

140.2 |

144.8 |

|

Initial fees collected in the year and deferred |

13.1 |

12.7 |

|

Income amortised during the year to fees income |

(15.8) |

(17.3) |

|

|

137.5 |

140.2 |

CONTRACT HOLDER Assets under administration

Contract holder assets under administration ("AuA") represent the net assets held to cover financial liabilities, as detailed in note 17 to the consolidated financial statements. These assets are selected by or on behalf of contract holders to meet their individual investment objectives.

The Group receives investment inflows into AuA from both single and regular premium contracts. These inflows are offset by withdrawals, policy charges, premium holidays on regular premium policies, and market valuation movements.

Reflecting the Group's international client base, most premium contributions are denominated in currencies other than sterling. At 30 June 2025, the currency composition of AuA remained broadly consistent with the prior year, with 74% denominated in US dollars (2024: 73%) and 7% in euros (2024: 7%).

From time to time, certain collective investment schemes linked to customer contracts may become illiquid, suspended, or enter liquidation. In such cases, the Directors apply judgement in determining the fair value of these assets. The cumulative impact on the balance sheet is not material.

At 30 June 2025, the value of AuA stood at £1,129.8m, a decrease of 1.9% from the prior year (2024: £1,150.9m). This reduction reflects lower regular premium inflows and adverse market and currency movements, partially offset by higher single premium contributions and reduced withdrawals.

|

|

2025 |

2024 |

|

|

£m |

£m |

|

Deposits to investment contracts - regular premiums |

64.4 |

74.4 |

|

Deposits to investment contracts - single premiums |

54.5 |

33.9 |

|

Withdrawals from contracts and charges |

(167.2) |

(173.3) |

|

Effect of market and currency movements |

27.1 |

114.4 |

|

Movement in year |

(21.2) |

49.4 |

|

Opening balance |

1,150.9 |

1,101.5 |

|

Closing balance |

1,129.8 |

1,150.9 |

The analysis of AuA held by each Group subsidiary to cover financial liabilities is as follows:

|

|

2025 |

2024 |

|

Fair value of AuA at 30 June |

£m |

£m |

|

|

|

|

|

|

1075.7 |

1,091.6 |

|

Hansard |

54.1 |

59.3 |

|

|

1,129.8 |

1,150.9 |

Assets supporting the financial liabilities of Hansard Worldwide are held by

Since closing to new business in 2013, Hansard Europe's AuA has continued to decline in line with expectations, as contracts mature or are surrendered.

DIVIDENDS

An interim dividend of 1.8p per share was paid in April 2025, amounting to £2.4 million.

The Board has recommended a final dividend of 2.65p per share (2024: 2.65p), subject to shareholder approval at the Annual General Meeting. If approved, the dividend will be paid on 13 November 2025, bringing the total dividend for the year ended 30 June 2025 to 4.45p per share (2024: 4.45p).

complaints and potential litigation

Financial services institutions may become involved in disputes where the performance of assets selected by or on behalf of contract holders-typically through their advisers-fails to meet expectations. This is particularly relevant for complex products distributed across

Although the Group has never provided investment advice, as this responsibility lies with the contract holder or their appointed adviser or agent, it has nonetheless received complaints regarding the performance of assets linked to certain contracts. Most cases have arisen in

As at 30 June 2025, the Group had been served with writs representing a net cumulative exposure of €23.8m (£20.4m) (2024: €23.8m / £20.2m), relating to contract holder complaints and asset performance issues. These exposures are disclosed as contingent liabilities in note 26 to the consolidated financial statements.

During the year, the Group successfully defended three cases with combined exposures of approximately £0.4m, one of which is subject to appeal (2024: successfully defended eight cases with exposures of £1.3m).

In line with Group policy, contingent liabilities are maintained even where cases have been won at first instance, and if they are subject to appeal-this includes the Group's largest single case in

During the year, £0.4m was recovered in relation to litigation expenses (2024: £0.7m), and further recoveries are anticipated as claims progress.

While the final outcome of these cases cannot be predicted with certainty, based on legal advice and past experience the Group believes it has a strong chance of success in defending the majority of claims and expects that a number of the larger claims will be ultimately mitigated by insurance cover.

Except for smaller cases where (based on historical patterns) settlements may be likely, all writs have been treated as contingent liabilities and disclosed accordingly. Where a consistent pattern of settlement exists for a group of claims, a provision has been made for the remaining exposures and included in note 20 'Provisions', to the extent they can be reliably estimated.

Net asset value per shaRE

The net asset value per share on an IFRS basis as at 30 June 2025 is 12.0p (2024: 15.1p) based on the net assets in the Consolidated Balance Sheet divided by the number of shares in issue, being 137,557,079 ordinary shares (2024: 137,557,079).

FUTURE PROSPECTS

As we enter FY26, the Group is well positioned to build on the strategic and financial momentum established over the past year. FY25 marked a period of consolidation and execution, with the successful launch of Global Select, Ascend, and Future Focus, alongside the embedding of our new policy administration system. These initiatives have laid a strong foundation for scalable growth, operational efficiency, and enhanced client outcomes.

Looking ahead, our strategic priorities are anchored in three imperatives: Improve, Grow, and Future-proof. These guide our investment decisions and operational focus across the Group.

· Improve: We will continue to enhance our proposition through product refinement, service excellence, and digital enablement. Initiatives such as the extension of the fund range, the introduction of new product features, and the elevation of service standards are already underway.

· Grow: FY26 will see the launch of our Japanese proposition through our partnership with Guardian, marking a significant milestone in our international expansion. We are also deepening our presence in

· Future-proof: We are investing in technology and advancing governance and sustainability initiatives to ensure long-term resilience. Another full-year impact of depreciation from our new policy administration system will be reflected in FY26 results, but this is expected to be offset over time by operational efficiencies and cost savings.

From a financial perspective, the Group remains well capitalised and committed to disciplined capital management. While macroeconomic headwinds-including potential interest rate declines, currency volatility, and inflationary pressures-may place short-term pressure on IFRS profitability, our underlying fundamentals remain strong. The Group's solvency position is robust, supported by a conservative investment strategy and a prudent provisioning approach. Regulatory solvency cover, a key measure of dividend-paying capacity, is expected to remain well above minimum requirements.

While we expect fee income to benefit from equity market performance and the impact of our new proposition suite, we recognise that fees generated by older, higher-margin products are running off. As a result, sustaining or growing overall fee income will depend on the continued success and scale of our newer product suite, market expansion, and distributor relationships. Investment income is also expected to benefit from proactive capital, revenue, and treasury management. While operating cash flows were lower in FY25 due to strategic investment, we anticipate an increase in cash generation as new business momentum builds and cost efficiencies are realised.

In summary, FY26 represents a pivotal year in our strategic and financial journey. With a refreshed product suite, enhanced digital infrastructure, expanding international footprint, and a clear focus on sustainability and capital strength, the Group is well placed to deliver long-term, responsible growth and sustainable value for all stakeholders.

Risk management and internal control

The Group continues to operate a comprehensive Enterprise Risk Management Framework, reflective of the Board's focus on effective risk management as an integral element of corporate success. The ERM Framework sets out the governance arrangements, principles, guidelines, practices and standards for risk management and internal control, which cumulatively ensure that the business is robustly prepared to identify, understand, and navigate the uncertainties and risks which it may encounter, and which can either pose threats or offer opportunities. The ERM Framework ensures that all such threats and opportunities, whether actual or emerging, are identified, assessed, monitored, managed, and reported using structured, consistent, and comprehensive methodologies. These arrangements seek to embed risk management within strategic decision-making and business planning activities and to continuously shape organisational values and culture. The maturity of the ERM Framework and its capacity to respond quickly to emerging risks and adapt to changes arising via the internal or external environment, ensure that risk management and internal control remain central to the Board's oversight, direction and control of the Group, and support informed decision making and sound business practices.

Approach

Having regard to the

· Support the Board's determination of the nature and extent of the Group's principal risks and the boundaries of risk appetite governing the pursuit and achievement of strategic objectives.

· Inform the Board's understanding and assessment of existing, evolving, and emerging risks, together with combinations of those risks in the form of plausible stresses and scenarios, which have the potential to threaten the Company's business model, future performance, solvency, liquidity, operational resilience, regulatory standing, or reputation. This includes analysis of the likelihood, impact, and time horizon over which such risks, or combinations of risks, might emerge or crystallise and determining how such risks should be managed or mitigated to reduce their likelihood or impact.

· Facilitate the effective and efficient operation of the Group and its subsidiary entities by enabling a consolidated and comprehensive approach to the management of risks across the Group, with specific attention to aggregate impacts and effects, enabling appropriate responses to significant business, operational, financial, compliance and other risks to business objectives, so safeguarding the assets of the Group.

· Help to ensure the quality of internal and external reporting. This requires the maintenance of proper records and processes that generate a flow of timely, relevant, and reliable information from within and outside the Group, enabling the Board to form their own view on the effectiveness of risk management and internal control arrangements through the regular provision of relevant information and assurances.

· Seek to ensure continuous compliance with applicable laws and regulations as well as with internal policies governing the conduct of business.

· Drive the cultural tone and expectations of the Board in respect of governance, risk management and internal control arrangements and the delegation of associated authorities and accountabilities.

The ERM Framework has been designed to be appropriate to the nature, scale, and complexity of the Group's business at both corporate and subsidiary level. The ERM Framework components are reviewed on at least an annual basis and refined, if necessary, to ensure they remain fit for purpose in substance and form and continue to support the Directors' assessment of the adequacy and effectiveness of the Group's risk management and internal control systems. Such assessment depends upon the Board maintaining a thorough understanding of the Group's risk profile, including the types, characteristics, interdependencies, sources, and potential impact of both existing and emerging risks on an individual and aggregate basis.

Work is in active progress to review, update and enhance the ERM Framework, where necessary, in preparation for the principal changes introduced by the

Risk governance arrangements

The Board retains ultimate responsibility for the ERM Framework and its effective operation, and the Directors are responsible for determining, evaluating, and controlling the nature and extent of the risks which the Board is willing to accept across the spectrum of risk disciplines. The Board has formally delegated certain responsibilities in respect of internal controls and risk management to the Audit and Risk Committee. These responsibilities are defined within the Committee's terms of reference and provide for a range of important oversight and scrutiny protocols including: