AIM-listed firm published a 6.5% drop in reported EPS, but 15% growth in adj EPS

Companies: IQE plc

AIM-listed semiconductor manufacturer IQE delivered solid final results on Tuesday morning, but saw its share price take a c.12% hit after the market appeared to ignore the fact that adjusted numbers showed EPS growth of +15% (from 2.6p to 3.0p), and focused on the reported numbers that show a drop in EPS of 6.5% (from 2.9p to 2.7p).

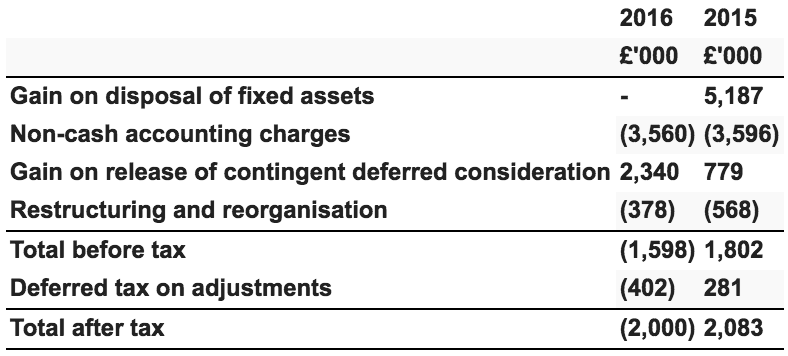

Below is the table describing the adjustments made in reaching the adjusted numbers. It shows that in 2015, the results were adjusted down c.£2m, and then 2016 saw a roughly offsetting adjustment up. This is reassuring because constant upward adjustments would be a red flag.

There is a hefty level of share-based payments embedded in the £3.5m of non-cash accounting charges that looks to be stripped out each year. If these payments, which are probably the issue of shares or share options, occur every year, there is an argument not to strip them out of underlying numbers. However, given the charges are the same across both years, this isn't affecting the change in adjusted numbers.

The main drivers for the upward adjustment in 2016 and downward adjustment in 2015 both appear completely reasonable in our view:

2015 numbers were flattered by a £5m gain on a disposed fixed asset. If that hadn't occurred, PBT would have been around £14m rather than the £19m that was reported.

2016 numbers included a gain related to a contingent deferred consideration for a prior acquisition. This future payment was provisioned for on the balance sheet but now does not need to be paid. Again, it seems sensible to strip this out. If this hadn't occured then PBT for 2016 would have been around £16.7m

Therefore PBT would have grown from c.£14m to c.£16.7m in the absence of these one-off gains, which justifies the adjustments made.

Adjusted numbers can be a menace when they mask true performance. However, reported numbers can be equally misleading if sensible adjustments aren't made.

Looking at cash generation, operating cash flow rose 5% over the year from £19.1m to £20.1m, which is more in line with the movement in adjusted earning numbers rather than reported earnings numbers.

The results were c.4% ahead of N+1 Singer's expectations, which were upgraded in December. The Broker was positive about today's update, saying the key Wireless and Photonics markets grew strongly, licence income outperformed expectations, and that it expected the positive momentum to continue.

"...prompting c.5- 10% EPS upgrades, although we see scope for more material upgrades over the course of our forecast horizon. IQE is one of our key picks for the year. The shares have risen 45% YTD but with today’s results triggering upgrades and further positive newsflow expected, we believe there is more to go for. Buy."