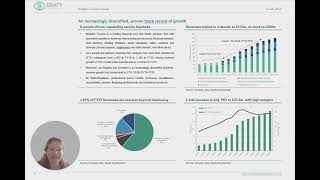

Begbies Traynor’s FY25 results convincingly illustrate the strength of its multi-disciplinary professional advisory team. FY25 revenue rose 12% to £153.7m, including 10% organic growth, and Adj. PBT margin remained high at 15.3%. FCF pre acquisitions of £19.4m funded acquisitions, share buy-backs and progressive dividends.

Moreover, the macro-economic environment continues to be supportive and with an increased insolvency order book management is confident in FY26E growth. Approximately 55% of revenues come from business recovery advice and the insolvency order book has increased 9% to £78.6m at the end of April 2025.

Strategic expansion to over 1,300 colleagues has enabled the Group to take on larger and more complex insolvency cases as well as expand its financial advisory, property consultancy and property auction services (among others).

Despite recent strength, BEG shares still trade at a 30% discount to long-run average valuation multiples and a discount to peers. With highly profitable organic growth and free cashflow to fund both acquisitions and dividends, we see scope for a material rerating.

Our fair value / share remains at 150p.