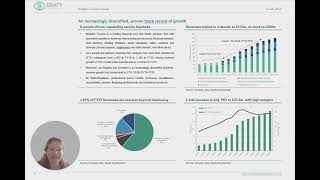

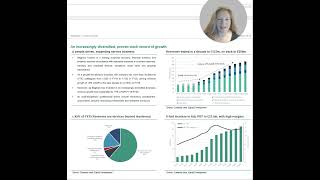

Begbies Traynor has concluded FY25 with a very strong performance. 12% revenue growth in FY25, from its multi-disciplined suite of services, has led to 7% growth in Adj. PBT and £19.4m in FCF pre-acquisitions (above expectations). Moreover, the macro-economic environment is supportive, and the pipeline of potential acquisitions is encouraging.

FY25 revenue growth of c.12% to £153m was c.1% above consensus expectations. An impressive c.11% organic growth in Business recovery and advisory services to c.£107m sales, reflects Begbies’ ability to advise on larger corporate restructurings as well as recruit senior professionals. Meanwhile Property advisory and transactional services grew revenues 15% (including 7% organically) to c.£46m, also reflecting hires across multiple services.

Despite cost headwinds, Begbies maintained its divisional margins of 26% and 17% in 2H25, leading to Adj EBITDA +10% to £31.3m, Adj PBT +7% to £23.5m and free cashflow of £19.4m pre-acquisitions. This was c. £5m better than expected, in part due to excellent working capital management.

Begbies trades at a c. 35% discount to its long-run average valuation multiples and a discount to peers. With highly profitable organic growth of 5%-6%, and free cashflow to fund both acquisitions and dividends, we see scope for a material rerating from only 8.6x cal 2026 PER.

We raise our PBT estimates and our fair value/share moves up from 145p to 150p.