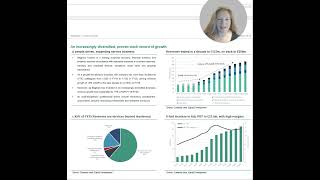

Begbies Traynor has confirmed financial performance in 3Q25 was as expected and that FY25E will extend its track record for strong financial growth. We forecast 11% revenue growth and a high 15% Adjusted PBT margin. The macro-economic environment remains supportive for Begbies and the group’s expansion into property advisory gives momentum which we believe is undervalued, trading on only c.9x calendar ‘25 PER.

Today’s trading update confirms that “both divisions have been consistent with the Board’s expectations in the quarter” and that “with a strong pipeline and continued elevated activity levels, our expectations for the full year remain unchanged”. We forecast revenue of £152m for FY25E, +11%, comprising 9% for Business Recovery and Advisory services (to £105m) and 17% for Property Advisory services (to £47m).

BEG shares trade at a c.35% discount to their long-run average valuation multiples and a discount to peers. Offering highly profitable organic growth of 5%-6%, we see scope for a significant rerating to 14x calendar ‘25 PER and a 3% yield – equating to a fair value of 145p / share.