BTG Consulting has announced good Q3'26 trading, with the business on track for FY26E market expectations. As anticipated given the tough macro-economic backdrop, restructuring services has continued to win new instructions whilst, encouragingly, financial advisory has completed on a greater number of transactions in recent weeks.

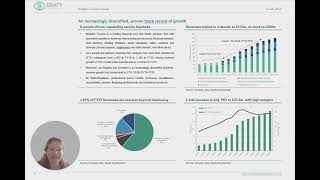

Q3’26 has been in-line with group expectations. Following 7% group revenue growth in H1’26 Restructuring services has continued to benefit from new instructions as the tough macro-economic environment is causing some businesses to struggle. Meanwhile the financial advisory team completed more transactions in Q3'26 (compared to H1'26 when some transactions were delayed) and have an 'encouraging order book' going into Q4.

The real estate advisory business has also performed in-line with expectations in Q3'26 after 7% revenue growth and c.25% profit growth in H1'26. Extending the group’s successful acquisition track record, the integration of both Kirkby Diamond and Network Auctions is progressing according to plans.

We make no changes to our estimates and, despite good operational performance, BTG’s shares trade c.30% below their long-run average valuation multiples. With profitable organic growth of 5%-6% and free cashflow for both acquisitions and dividends, we see scope for a material rerating.

Our fair value remains 150p / share.