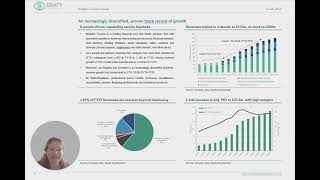

BTG Consulting has announced an excellent end to FY26, with revenue rising c.10% to £169m, c.2% above consensus expectations. This included 8% organic growth and has resulted in a c.6% increase in adj. PBT versus FY25, c.4% ahead of estimates.

The macro-economic environment continues to be tough for many companies following the Middle East conflict. We raise our estimates to reflect BTG’s multi-disciplined growth, its increased pipeline of restructuring engagements, and demand for its advisory services.

BTG offers profitable organic growth, c.15% adj, PBT margins, a strong balance sheet with only £1m net financial debt (FY26E), and free cashflow for both acquisitions and dividends, which to us justifies a rerating.

We raise our fair value per share from 150p to 170p, which equates to a 6% cal 2027 FCF yield and 14x cal 2027 PER, in line with historic trading averages.

21 May 26

BTG Consulting plc: FY26 Trading Update - Diversified, high organic growth drives upgrades - 21 May 2026

BTG Consulting plc: FY26 Trading Update - Diversified, high organic growth drives upgrades - 21 May 2026

-

-

-

54 views

-